I want to start with something that stopped me mid-scroll yesterday morning.

Mark Cuban — the billionaire who once said he would “never sell” his Bitcoin, who called it “better than gold,” who had 60% of his entire crypto portfolio sitting in BTC — just revealed he sold most of it.

Not quietly. Not through some obscure filing. He said it out loud on a podcast, explained exactly why, and used language that will make Bitcoin maximalists furious.

“Bitcoin has lost the plot,” he said. “It’s been disappointing.”

Now before you either panic sell or dismiss this as one billionaire’s irrelevant opinion — I want to walk through what Cuban actually said, why his reasoning has a flaw that most coverage missed, and what this whole episode reveals about the ongoing debate around Bitcoin’s real identity.

Because this is not just a celebrity selling a coin. This is a genuinely interesting argument about what Bitcoin is supposed to be.

What Cuban Actually Said — The Full Picture

Cuban, whose net worth is about $10 billion, said Bitcoin’s price behavior during the recent Iran conflict challenged one of the core reasons he owned the asset — during an episode of the “Portfolio Players” podcast, where he mainly discussed professional sports and his ownership of the Dallas Mavericks.

The quote that is going to define this story:

“When all this shit hit the fan with the Iran war(Source: CoinDesk) , Bitcoin was always the best alternative to fiat currency losing its value and I always thought it was a better version of gold than gold. Well, gold just blew up… Bitcoin dropped. And every time the dollar dropped, Bitcoin should’ve gone up… and it just didn’t do that.”

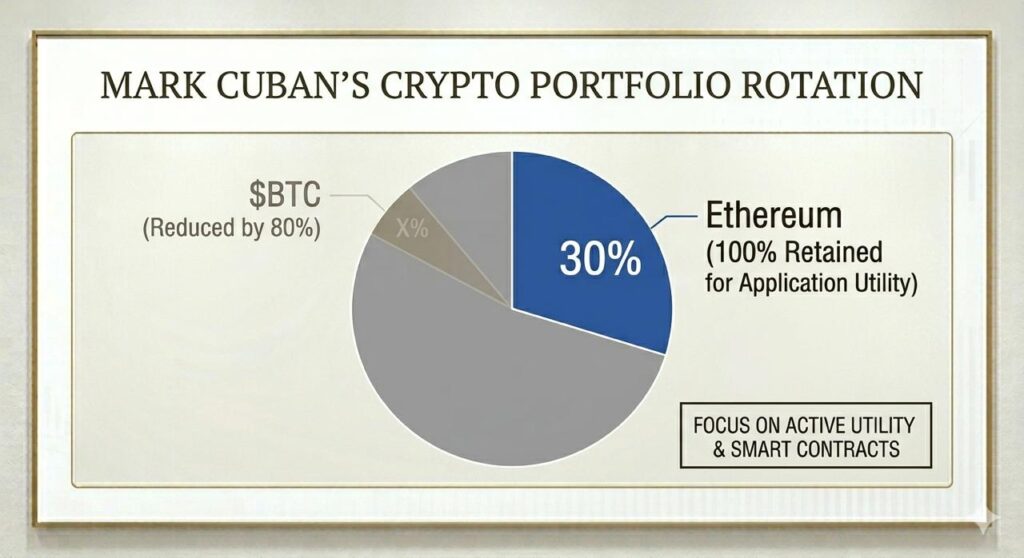

Cuban’s portfolio heading into 2026 was roughly 60% Bitcoin, 30% Ethereum and 10% other assets. He once said he had “never sold” his Bitcoin and described scarcity as making it superior to gold. That conviction has now reversed.

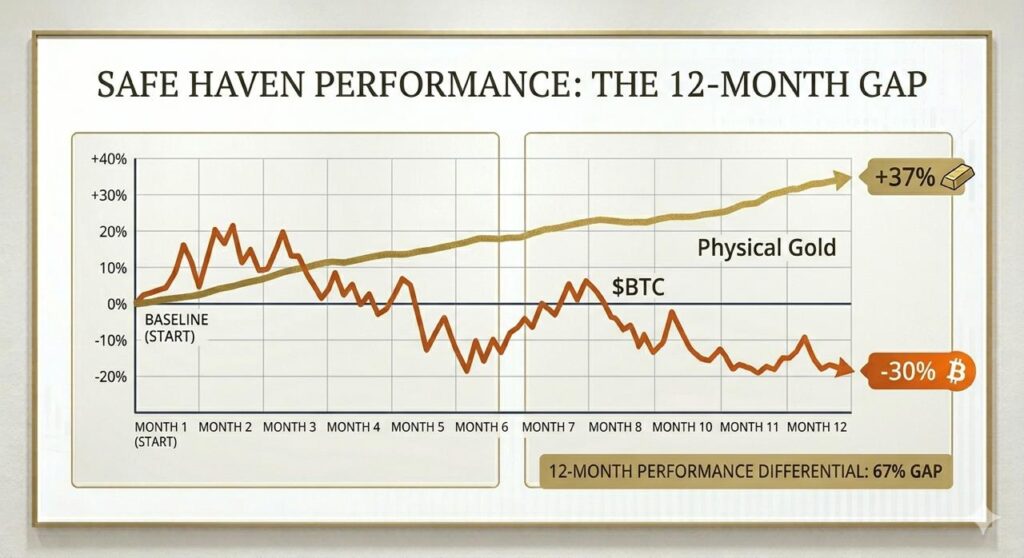

During US-Iran tensions, Bitcoin analysis showed it underperformed gold, which reached $5,500 per ounce. Bitcoin declined 30% over 12 months, while gold rose 37%.

So his argument is straightforward. He bought Bitcoin because he believed it would behave like digital gold — rising when the dollar weakened, rising when geopolitical tension increased, serving as a safe haven when traditional markets struggled. When that thesis was tested in real market conditions, Bitcoin did not deliver what he expected.

Cuban also expressed dissatisfaction with cryptocurrency in general, arguing it hasn’t come up with an “application for grandma.” He referred to memecoins as “garbage.” (via Benzinga)

He was not done there. Cuban still supports Ethereum, citing its real-world use cases such as decentralized finance and on-chain applications. He described himself as less disappointed in Ethereum because it is still supported by genuine utility.

The Flaw in Cuban’s Argument — And It Is a Real One

Here is where I need to be honest about something most coverage of this story glossed over entirely.

Cuban’s thesis rests on a specific timeframe. And when you look at a different timeframe, his argument actually falls apart.

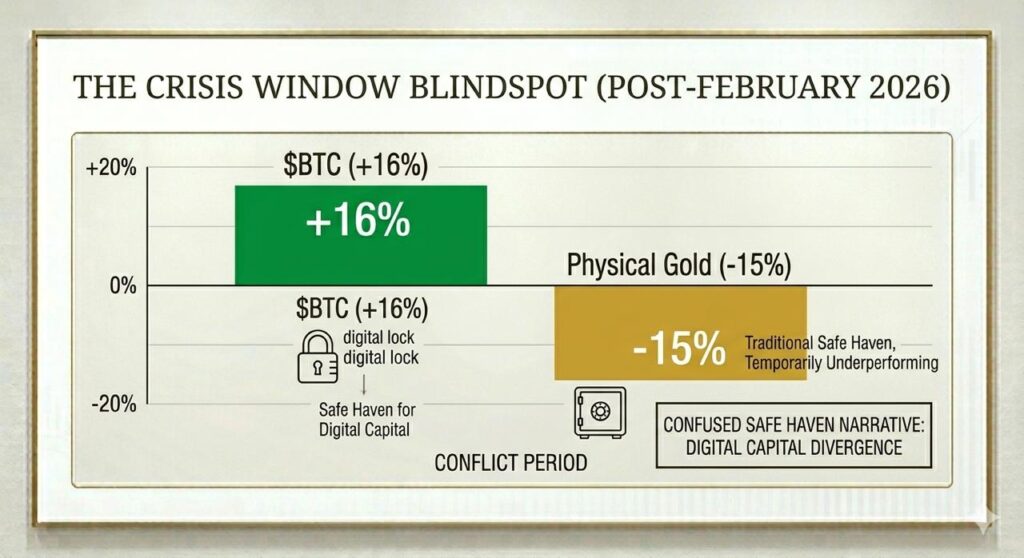

Bitcoin has risen more than 16% since the first signs of the US-Iran conflict emerged in late February 2026. During that same period, gold fell more than 15%. This means Cuban may be comparing the wrong time windows.

Read that again. During the actual Iran conflict period — the specific geopolitical event he cited as proof Bitcoin failed — Bitcoin outperformed gold by over 30 percentage points.

In the past 12 months, Bitcoin has been down roughly 30% while gold has been up 37%. But during the Iran conflict specifically, Bitcoin outperformed gold. So while Bitcoin did not behave as expected over the full 12-month window, it did better than gold during Cuban’s own timeline of the Iran conflict.

This matters because Cuban presented his argument as if Bitcoin failed during the geopolitical crisis. But the data suggests Bitcoin actually performed better than gold during that specific crisis. His disappointment appears to be based on the 12-month window, not the conflict window he described.

This does not mean Cuban is wrong to sell. He can sell whatever he wants for whatever reason he wants — it is his money. But the specific argument he made on the podcast does not fully hold up when you look at the actual data from the period he referenced.

What This Tells Us About Bitcoin’s Identity Problem

Setting aside whether Cuban’s data reading is accurate, his frustration points to something real that the Bitcoin community has been debating for years.

What exactly is Bitcoin?

There are at least three competing narratives that have existed simultaneously for most of Bitcoin’s life, and they have very different implications for how the asset should behave.

Bitcoin as digital gold. This is the narrative Cuban bought into. Fixed supply, decentralized, resistant to government control — properties that should make it an inflation hedge and safe haven. This is the narrative that attracted many early institutional adopters and is still the dominant framing in mainstream finance discussions.

Bitcoin as a risk asset. The market, for much of the past few years, has treated Bitcoin less like gold and more like tech stocks. When risk appetite is high, Bitcoin goes up. When fear rises and investors sell risk assets, Bitcoin goes down. This behavior is completely inconsistent with the digital gold narrative but is empirically what has happened in many market stress events.

Bitcoin as a new asset class entirely. Some argue Bitcoin should not be compared to gold at all — that it has its own cycle, its own dynamics, and judging it by how well it hedges dollar weakness is applying the wrong framework entirely.

Cuban bought Bitcoin with the first narrative in mind. When the market treated it according to the second narrative, he concluded the first narrative was wrong and sold. That is a completely rational response to a thesis being invalidated — even if the specific data point he cited is debatable.

Why Cuban’s Move Matters Beyond Just His Portfolio

When someone like Mark Cuban sells Bitcoin and explains why publicly, it has ripple effects that go beyond one person’s investment decision.

Cuban warned his move could weaken institutional confidence in Bitcoin as a safe-haven and prompt reassessment of crypto allocations.

Cuban has been one of the most mainstream-accessible advocates for crypto. He appeared on Shark Tank for years. He owned the Dallas Mavericks. He is recognizable to people who have never bought a single cryptocurrency. When he publicly shifts his position, it reaches an audience that does not follow crypto media daily.

The concern is not that one billionaire sold some Bitcoin. The concern is the narrative he attached to the sale. If the “digital gold” story starts losing credibility among mainstream investors who bought it for that specific reason, it could affect demand from exactly the type of investor Bitcoin needs to attract institutional capital at scale.

This is why the data correction matters. If Cuban’s argument is based on a misreading of the timeframe, then the narrative damage could be based on faulty reasoning — and addressing that publicly is worthwhile.

What the Bitcoin Community Is Saying Back

The response from Bitcoin advocates has been predictable in some ways and interesting in others.

The standard response is that short-term price behavior does not invalidate a long-term thesis. Gold took decades to establish its safe-haven status through consistent behavior across multiple crises. Bitcoin is 16 years old. Judging its safe-haven credentials based on behavior during one conflict over one year is, the argument goes, applying an unreasonably short timeframe.

The more substantive response points to the data flaw I mentioned earlier. If Bitcoin actually outperformed gold during the Iran conflict period, then Cuban’s specific complaint does not match the evidence from the period he cited.

Bitcoin defenders note the asset has risen more than 16% since the first signs of the US-Iran conflict, countering Cuban’s narrative on the timeframe.

There is also the argument that Bitcoin’s behavior is still maturing as an asset class. Institutional adoption through ETFs only became mainstream in 2024. The regulatory framework that would allow truly broad institutional allocation — the Clarity Act — is still working its way through Congress. Judging Bitcoin’s safe-haven properties before that infrastructure is fully built may be premature.

None of these responses definitively prove Cuban wrong. They just suggest the picture is more complicated than his podcast comments implied.

What About Ethereum — Cuban’s Remaining Bet

One detail worth paying attention to is what Cuban kept.

He sold most of his Bitcoin. But he kept his Ethereum.

Cuban said he is less disappointed in Ethereum because it is still supported by real-world use cases such as decentralized finance and on-chain applications.

This is a meaningful distinction. Cuban’s critique of Bitcoin is essentially that it failed to do what it was supposed to do — hedge against dollar weakness and geopolitical risk. His continued faith in Ethereum is based on something different — actual utility. Smart contracts, DeFi, on-chain applications. Things that exist and work regardless of whether Ethereum performs as a safe-haven asset.

This suggests Cuban’s investment philosophy has shifted from narrative-based investing — buying Bitcoin because of the digital gold story — to utility-based investing — holding Ethereum because it enables applications that actually function.

Whether that framework will prove correct is another question entirely. Ethereum has its own complicated relationship with its price performance versus its utility. But the distinction Cuban draws is worth understanding.

What This Means For Regular Crypto Investors

I want to be careful here because I think there is a risk of drawing the wrong lesson from this story.

The wrong lesson is: Mark Cuban sold Bitcoin, therefore you should sell Bitcoin.

Cuban had specific reasons based on a specific thesis he had built around Bitcoin’s hedge properties. If you hold Bitcoin for different reasons — long-term store of value, exposure to a new asset class, belief in decentralized money — his reasoning does not automatically apply to your situation.

The more useful question to ask is: why do I hold Bitcoin, and has anything happened to invalidate that reason?

If you bought Bitcoin because you believe it will act as a safe-haven during dollar weakness and geopolitical tension — Cuban’s experience is relevant data for your thesis. You should examine it seriously.

If you bought Bitcoin because you believe in its long-term adoption trajectory, its fixed supply as a hedge against monetary inflation over decades, or its role as a settlement layer for a new financial system — Cuban’s 12-month performance disappointment is much less relevant to your thesis.

Investment theses need to be tested against evidence. Cuban tested his and found it lacking. That is actually good investing practice — being willing to change your mind when the evidence challenges your assumptions. The question is whether the evidence he is citing actually supports the conclusion he drew, and as I noted, there is reason to question that.

The Bigger Picture — On Bitcoin Pizza Day

There is something almost poetic about this story breaking on Bitcoin Pizza Day.

Sixteen years ago today, 10,000 Bitcoin bought two pizzas. The people who call that the worst trade in history miss the point — that transaction helped establish Bitcoin’s real-world value and started the process of price discovery that eventually led to Bitcoin trading above $77,000 today.

Bitcoin has survived countless billionaires dismissing it, selling it, or declaring it dead. It has survived regulatory crackdowns, exchange collapses, 80% drawdowns, and years of mainstream skepticism.

Mark Cuban selling 80% of his Bitcoin is meaningful news worth analyzing seriously. But it is one data point in a 16-year story that has consistently surprised the people who wrote it off.

Whether that story continues to surprise depends on whether Bitcoin eventually delivers the safe-haven properties Cuban and others expected — or whether it finds a different identity that proves equally or more valuable.

That question remains open. And on Bitcoin Pizza Day, in the 16th year of this experiment, that open question is part of what makes this asset so interesting to follow.

This article is for educational and informational purposes only. Nothing here constitutes financial or investment advice. Cryptocurrency markets carry significant risk of loss. Always conduct your own research and consult a qualified financial advisor before making any investment decisions.

You might like these contents:-

Is Crypto Still Worth It in 2026 — An Honest Look After All The Hype

and content creator with over 5 years of

hands-on experience in blockchain technology

and digital assets. He actively trades and

researches crypto markets daily, and shares

insights with over 110,000 followers on

Binance Square. He founded CrypBuzz.com to

provide honest, research-backed crypto

education for everyday investors.